Changes to UK accounting rules are on the horizon, the most notable of which will affect the way revenue and leases are accounted for [1]. Whilst these changes will take effect for accounting periods commencing on or after 1 January 2026, there is a backward-looking dimension with a requirement for your opening reserves to be adjusted [2] so as to reflect the position had the new rules always been in play, so it’s a good time to start thinking ahead.

We don’t expect the changes to heavily impact the revenue recognition polices for many recruitment companies, however it’s worth understanding the 5-step model that is to be introduced so that you can:

- Identify the relevant customer contract(s).

- Identify any/all performance obligations in the contract.

- Determine the transaction price (i.e. what you’re expecting a customer to pay for the services delivered).

- Allocate the transaction price to the performance obligations in the contract.

- Recognise revenue as and when the company satisfies a performance obligation.

We do however expect a widespread impact of the changes in accounting for leases. To re-cap, for operating leases currently, rent is (approximately) accounted for on a cash basis, the expense being taken to the profit & loss account when paid. With the new rules however, lessees need to recognise both a liability at the commencement date of the lease (which will be the present value of the lease payments that are to be paid over the lease term) and a matching, “right-of-use (ROU)” asset on the company’s balance sheet.

The discount rate used to determine present value should be the rate of interest implicit in the lease (this will likely be an estimate based on typical costs of debt). The ROU asset will initially be equal to the liability at the outset but will subsequently be depreciated over a period we’d expect to be commensurate with the term of the lease.

To illustrate the effect of these changes, we have looked at a simple example where we’ve assumed a property lease of 5 years, annual rent of £150,000 per annum, a 7% interest (discount) rate which gives rise to a present value of future lease payments of £615K, and a depreciation rate of 20% straight line over the 5 years.

Figure 1 – Liability Recognised on the Balance Sheet

Figure 2 – ROU Asset Recognised on the Balance Sheet

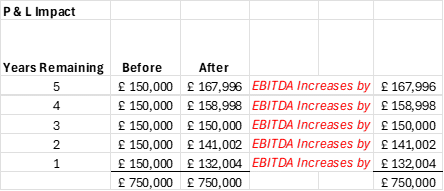

Figure 3 – Impact on the Profit and Loss Account (i.e. Depreciation plus Interest Expense versus Lease Expense)

Figure 4 – Impact on Balance Sheet Net Asset Value

Note: The impacts above are not cumulative. By the end of Year 5 the difference is £nil.

It’s worth saying that the consequences of these changes may be far reaching, for example:

- We may see lenders try to re-negotiate financial covenants as EBIT and EBITDA will suddenly have improved but not because of the company’s performance.

- On the flip side, companies may appear to be more highly geared as a liability suddenly pops up on the balance sheet.

- In terms of company size limits, we will see a new right of use asset appearing on balance sheets which will count towards the gross assets figure used for this purpose.

- Outcomes based on EBIT or EBITDA (e.g. bonus schemes, share plans) may be affected.

Company Size Thresholds

The UK government has recently confirmed changes to the criteria for assessing company size. A company’s size will generally[3] determine the financial reporting framework used, and whether or not the company requires a statutory audit.

When a company breaches at least two of these three criteria in two consecutive accounting periods, it moves up to the next size.

For accounting periods starting on or after 6 April 2025, the new size limits are to be as follows:

| Micro | Small | Medium | ||

| Turnover | After | £1m | £15m | £54m |

| Before | £632K | £10.2m | £36m | |

| Balance sheet | After | £500k | £7.5m | £27m |

| (Gross assets) | Before | £316k | £5.1m | £18m |

| Average employees | After | 10 | 50 | 500 |

| Before | 10 | 50 | 250 |

Whilst some companies may decide to dispense with an audit of their accounts as a consequence of these changes, it’s vital to consider the impact of that decision on all stakeholders – these might include lenders, credit rating agencies, customers and suppliers, all of whom may be inclined to place less reliance on the company’s reported results.

Other companies may see an opportunity to report under the much more straight forward FRS105 reporting standard for micro-entities. Again, there is much to consider before making a decision like this, not least what happens if and when the company goes back over the size limits due to growth.

The overall impact of these changes may well be the disclosure of less information in the public domain, but this will be a short-lived trend as there is other legislation making its way through which will require all companies to provide Companies House with a profit and loss account for every financial year!

Next Steps:

Given these significant changes, it’s essential for recruitment businesses to plan ahead. To discuss how these developments may affect your operations and to develop a strategy for compliance, please contact us or call 0845 606 9632 to speak with one of our experts.

[1] These being designed to bring UK reporting in line with International Financial Reporting Standards (IFRS)

[2] The revenue (not lease) changes allow you to amend comparative figures instead of amending the brought forward reserves.

[3] This isn’t always the case and it is necessary if the company is ineligible for exemptions for other reasons whether that’s in its own right or through membership of a wider group